You may have seen solar installers around Thailand advertising 0% credit card installment plans in 2026, some quoting monthly payments starting around ฿2,550. It's a genuinely useful option for some buyers — but before assuming it applies to your project, it helps to understand what these plans actually cover, and where a traditional financing route may fit a full-size system better.

What credit card installment actually covers

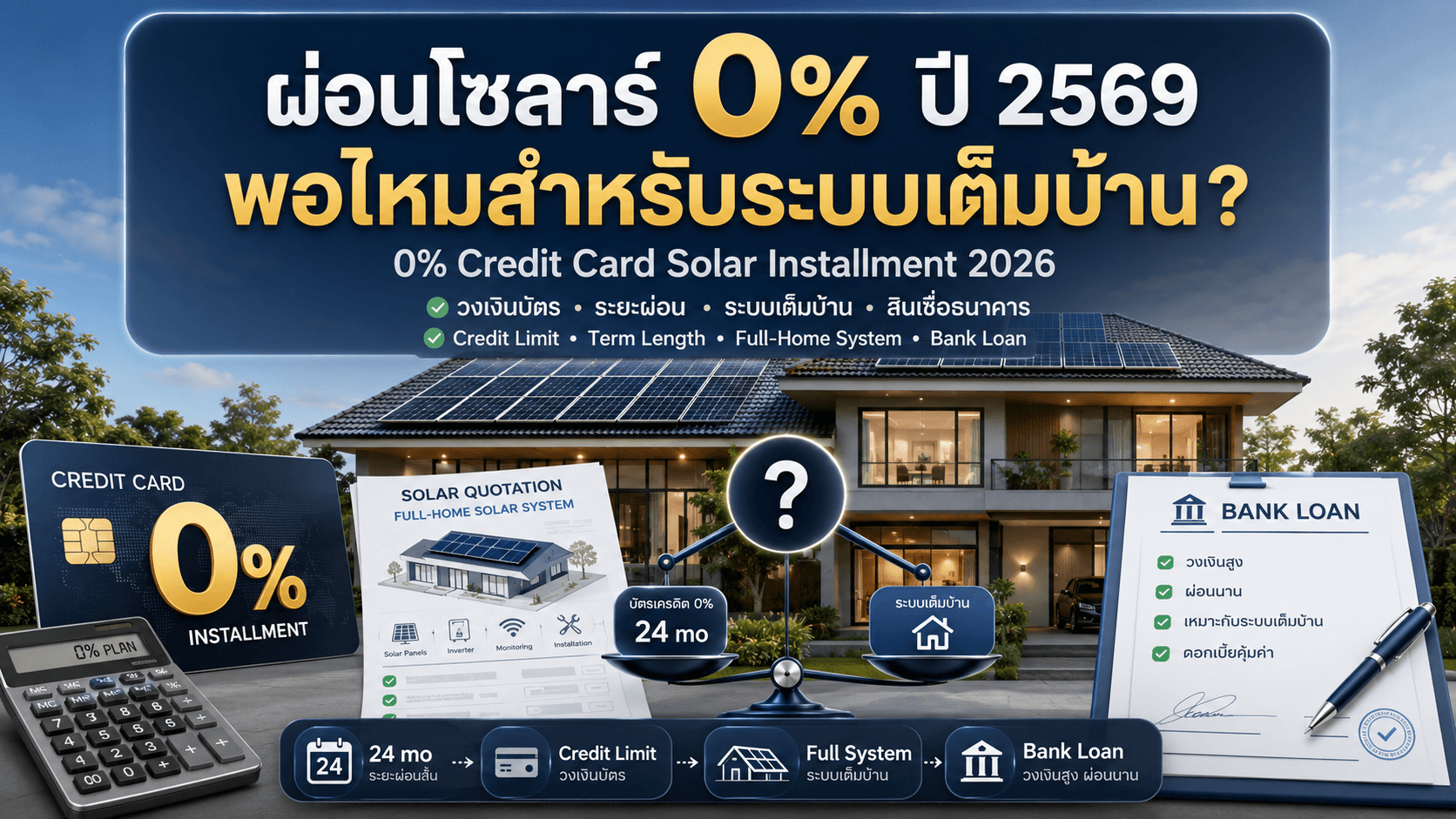

- Credit limits are set per cardholder, and typically leave room for purchases roughly in the ฿100,000–300,000 range for solar-sized transactions — well below what many full home or pool-villa systems cost.

- 0% installment terms are usually short — commonly 10 to 36 months — which pushes the monthly payment much higher than a longer-term loan for the same total amount.

- The merchant (the solar company) typically absorbs a fee to the card issuer for offering the 0% promotion — a cost that gets built into pricing somewhere.

Do the math on a real example: at a 24-month 0% term, a ฿300,000 system means ฿12,500/month — before accounting for whether that even fits under your card's available limit. A larger pool-villa or hotel system, often ฿400,000 and up, simply won't fit most personal credit limits at all.

Where bank financing fits better

- Bank loan terms typically run several years rather than months, which spreads the same total cost into a lower, steadier monthly payment.

- Loan amounts can be sized to match the actual cost of a full system, rather than being capped by a personal card's available credit.

- Bank financing does carry interest, unlike a 0% card promotion — so it's worth comparing the total cost of each option for your specific system size, not just the headline rate.

There's no single right answer — a 0% card plan can genuinely make sense for a small add-on (like a battery upgrade), while a full home or business system usually fits a longer-term loan better. The right choice depends on your system size and your card's available limit.

We help customers prepare and submit the paperwork for bank financing on full-size systems, so the monthly payment fits your budget without being squeezed into a short credit card term. Book a free consultation to talk through what fits your situation.

Frequently Asked Questions

Can I combine a credit card installment plan with a bank loan for the same system?

It's possible in principle — for example, financing a smaller add-on like a battery with a card while taking a loan for the main system — but it depends on how your installer structures the invoice and what each lender allows. Ask both the card issuer and the bank about splitting a purchase before assuming it works.

Is 0% installment really free, since the merchant pays a fee?

From the buyer's side, you genuinely pay no extra interest on a true 0% promotion — the fee the merchant pays to the card issuer is a separate cost to them, not something billed to you directly. Whether that cost is reflected elsewhere in the quoted price is worth asking your installer about directly.

What's the actual credit limit on my card for a purchase this size?

This varies entirely by cardholder and issuer, so there's no single number that applies to everyone. Check your available credit limit directly with your card issuer before assuming an installment plan will cover your system.